When you get into the back seat of an Uber, you don’t think twice about your safety or the administrative process of trying to file an insurance claim because you trust Uber’s vetting process. It’s only natural to assume that such a seamless experience — request ride, get ride, pay automatically — must have a simple claims process in the event of a crash. But understanding how Uber insurance works is crucial in the event of an accident.

If you’ve been hit or injured while riding in an Uber, you may wonder whether the page or platform to file a claim is accessible and straightforward. Sometimes, riders find themselves unable to proceed with a claim due to missing steps or being blocked from accessing necessary information. Make sure you are logged into your Uber account at the time of the incident, as this can be vital for taking swift action.

Uber’s insurance policy typically covers accidents while you’re in a ride, but filing a claim may require specific steps, such as submitting an email or contacting their support team. Their coverage is designed to protect passengers, but the actual process may vary depending on the circumstances. Understanding these details can help ensure that your claim moves forward smoothly and that you receive the compensation you deserve. If you’re uncertain, it’s always wise to consult with an expert to guide you through this process effectively.

How Uber Insures Drivers

Uber drivers are classified as “independent contractors,” which has countless implications for the degree of responsibility that Uber Technologies, Inc. has for the individuals using their app. As an independent contractor, an Uber driver is not an employee and is only using the app to connect with an individual who has requested a ride in the driver’s personal vehicle. This makes liability much different when compared to a taxi or limo driver, who is employed by a company and is under their insurance as long as they are operating a company vehicle or working for the company.

An Uber driver is only working with Uber (again, as an independent contractor) when they are logged into the app. Uber provides insurance benefits in increments depending on how the driver is using the app and whether or not they are actively providing a ride to a customer.

From Uber’s website:

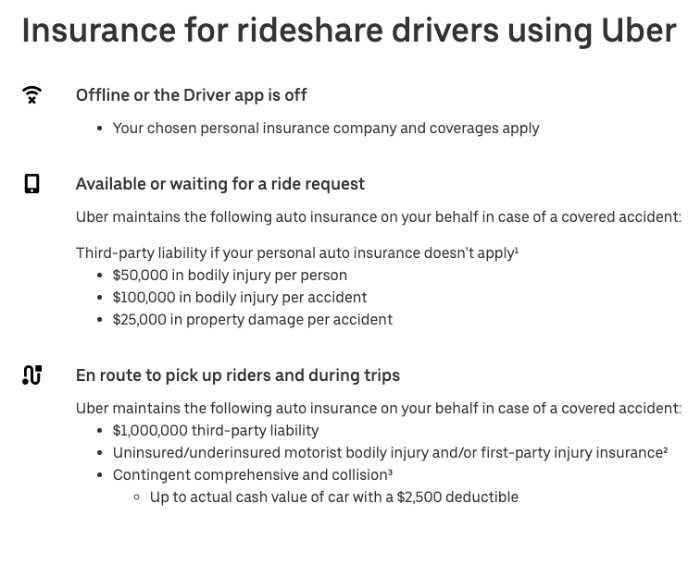

As you can see, a driver has no association with Uber when they are offline, or the Driver app is not turned on. In these instances, you will file an insurance claim with their personal insurance policy, just as you would with any other non-commercial driver.

If the driver has their Driver app turned on and is available to accept ride requests, then Uber provides them with limited coverage meant to supplement their personal insurance. This means that you will first file a claim against their personal policy, and if your damages exceed their limits, then you will follow a second claim with Uber’s insurance policy to recover the difference. The policy limits in this phase are $50,000 in bodily injury per person, $100,000 in bodily injury per accident, and $25,000 in property damage per accident.

When a driver accepts a ride, whether en route to pick them up or actively transporting a passenger, Uber’s insurance fully covers the driver and passengers. Third-party victims have access to up to $1 million in coverage for damages and will not need to file a claim with the driver’s personal insurance at all.

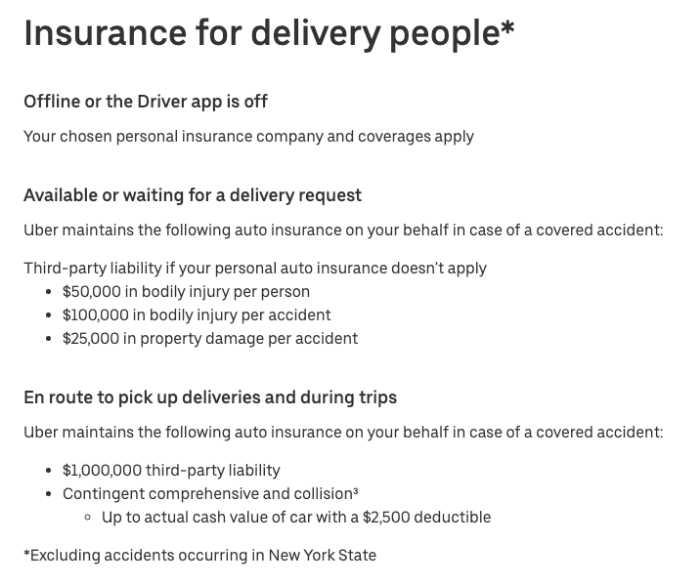

Uber delivery drivers have a similar graduated coverage arrangement with Uber, meaning that if the app is turned off, then they are solely covered by their personal insurance. If the app is on and they are waiting for a request, Uber’s policy will kick in if a claim exhausts all of their personal insurance coverage or their personal policy doesn’t apply. There are limits of $50,000 in bodily injury per person, $100,000 in bodily injury per accident, and $25,000 in property damage per accident.

When an Uber delivery driver has accepted a delivery and is either en route to picking up the order or in the process of delivering the order, then a victim in an accident will not need to file a claim against the delivery driver’s personal policy. Instead, much like an Uber driver’s protection, drivers are covered entirely by Uber’s insurance policy which has a policy limit of $1 million.

Remember: High Policy Limits ≠ Fair Settlements

Just because an insurance policy has a limit of $1 million does not mean that you will be able to automatically collect that full amount if you are in an accident with an Uber driver. Instead, the focus should be on the strength of your case and whether or not you have suffered damages that exceed the policy limits. Keep in mind that no matter the policy limit, an insurance adjuster’s goal while handling a claim is to settle said claim for as little as possible, as quickly as possible, while avoiding any future legal issues stemming from the accident. Your case will be no different.

Working with a personal injury attorney who has experience handling Uber accident claims can help you understand what your case may be worth and how to best proceed with the insurance company. Your Uber accident lawyer will fight for the maximum possible financial compensation to cover your damages, and will negotiate on your behalf to try and reach a fair settlement that meets your needs. If necessary, they will also take your case to trial to get the justice you deserve.

Contact Car Accident Attorney Now

The sooner you contact CarAccidentAttorney.com about your Uber accident, the sooner we can connect you with an experienced attorney in your area for a free consultation and case evaluation. During your consultation, you will have the opportunity to discuss the details of your accident, ask any questions you have about the legal process, and learn more about what to expect moving forward. The personal injury lawyers in the CarAccidentAttorney.com network operate on a contingency fee basis, which means that there is never any upfront cost or risk for you to hire a proven attorney, and they only get paid if they are able to recover financial compensation on your behalf. Contact CarAccidentAttorney.com, personal injury law firm directory to get started right away.